Who’s Preparing Your Taxes? The Shocking Truth About Unregulated Tax Preparers

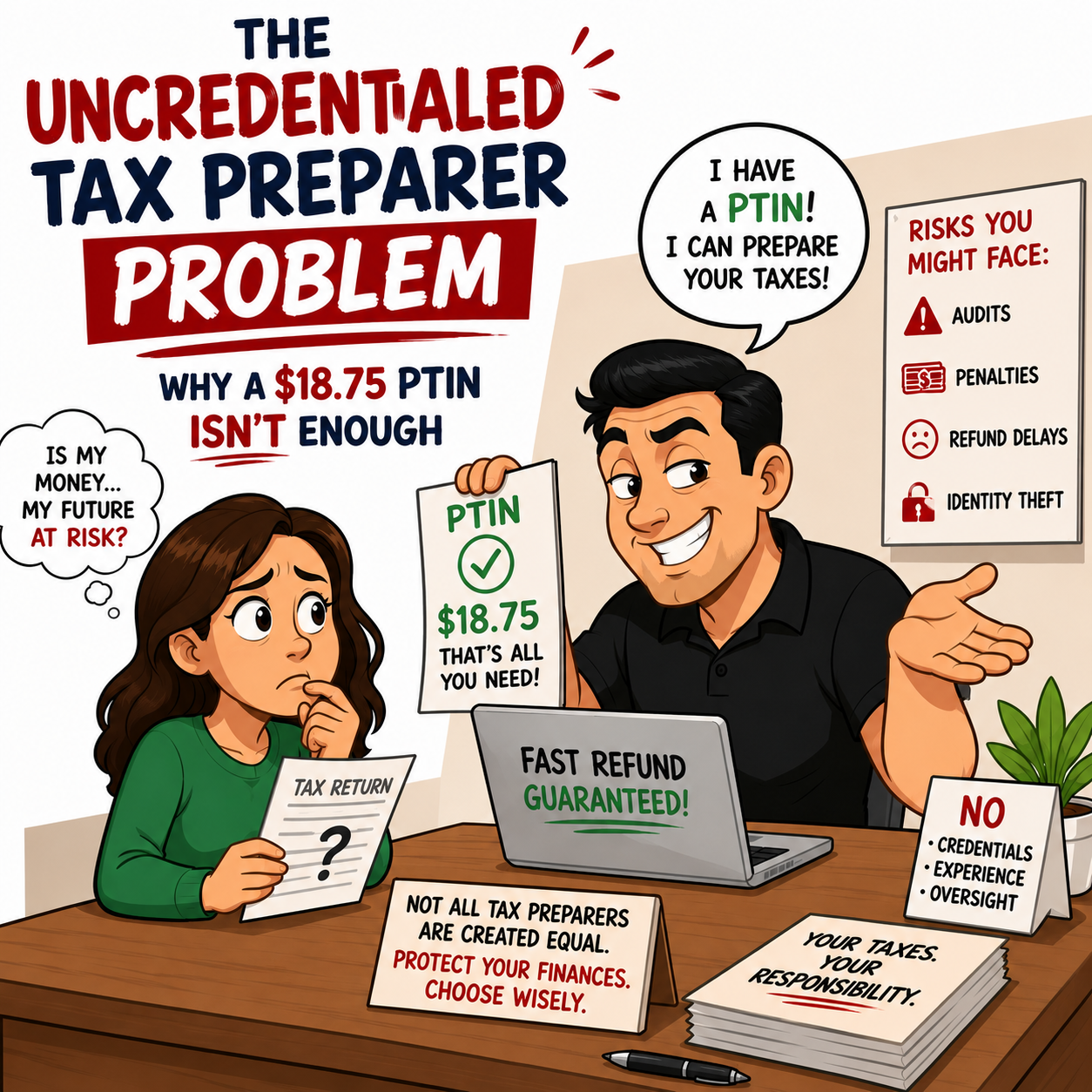

Every year, millions of Americans hand their most sensitive financial information to a stranger and trust that person to file an accurate, honest tax return on their behalf. What most taxpayers don’t realize is that virtually anyone can call themselves a “tax preparer” — with zero required education, zero competency testing, and no meaningful federal oversight beyond a $18.75 registration fee.

At GG CPA Services, we believe taxpayers deserve better. This post pulls back the curtain on the federal gap in tax preparer regulation, highlights the states that are stepping up — and names the bad actors who exploit the system at taxpayers’ expense.

The Federal “Standard”: A PTIN and a Prayer

At the federal level, the only hard requirement to prepare tax returns for compensation is obtaining a Preparer Tax Identification Number (PTIN) from the IRS. That’s it. The fee for 2026 is $18.75 — less than most people spend on lunch. There is no federally mandated competency exam. There is no required coursework. No background check. No demonstration of knowledge of the Tax Code.

The IRS does offer a voluntary option called the Annual Filing Season Program (AFSP), which encourages non-credentialed preparers to complete 18 hours of continuing education annually — including a 6-hour federal tax law refresher course, 10 hours of federal tax law topics, and 2 hours of ethics.

The consequences of this regulatory vacuum are stark. As of January 2026, a stunning 56% of the more than 684,000 preparers registered with the IRS were uncredentialed (note that as of May 2026 the active PTINs are 859,301) — meaning they were not attorneys, CPAs, enrolled agents, enrolled actuaries, or even AFSP participants. If we want to focus on CPAs, Enrolled Agents and Attorneys (credentialized) then the number drops to 300,882 (or around 35% of the PTIN holder total pool). And that figure almost certainly undercounts the true number, because “ghost preparers” — those who prepare returns but don’t sign them to avoid accountability — are invisible to IRS tracking.

What Uncredentialed Preparers Actually Do: The Data Is Damning

A major investigative report released in April 2026 by the Center for Taxpayer Rights used mystery shoppers to visit uncredentialed tax preparers in six states during the 2025 filing season. Testers posed as typical low-income filers with three common tax scenarios. The results were alarming.

The most problematic area by far was Schedule C income. Uncredentialed preparers routinely:

- Underreported cash income

- Estimated or completely fabricated deductions

- Confused rules around business use of the home

- Failed to ask basic questions about household composition and income

- Produced wildly inconsistent refund amounts for the same fact pattern

The downstream impact on the IRS’s books is enormous. According to IRS data cited in the report, returns prepared by uncredentialed preparers account for over 94% of the dollar adjustments in Earned Income Tax Credits (EITCs) for tax year 2021. For tax years 2018 through 2021, uncredentialed preparers accounted for 93% of all preparer penalties assessed and 89% of the dollar amount of those penalties.

States Are Filling the Federal Void

Because Congress has repeatedly failed to authorize mandatory minimum standards for federal return preparers, a handful of states have taken matters into their own hands. The regulatory landscape varies dramatically:

New York Sets the Gold Standard

New York’s framework stands out as the gold standard for state-level preparer regulation. Every paid preparer must obtain a NYTPRIN (New York Tax Preparer Identification Number) and include it on every return filed — a registration requirement that goes well beyond the federal PTIN. “Commercial” preparers who prepare 10 or more returns per year face an additional annual $100 registration fee — more than five times the federal PTIN cost — as well as mandatory continuing professional education (CPE) each year. Notably, CPAs, attorneys, and their employees who are already licensed elsewhere in the U.S. are exempt, recognizing that existing credentialing already imposes rigorous standards.

Oregon Goes Even Further

Oregon arguably has the most rigorous framework in the country, requiring a state-administered exam, an 80-hour qualifying education course, and 30 hours of annual CE. This is closer to what a true national standard should look like.

When “Preparers” Become Predators: Real Cases, Real Victims

The absence of federal standards doesn’t just mean sloppy returns. In some cases, it enables outright criminality. Here are two recent examples from our own backyard — and beyond — that underscore what is at stake.

Case 1: The New Jersey COVID Credit Scheme — $170 Million Stolen

Leon Haynes, a New Jersey tax preparer (not a CPA or EA), orchestrated the largest COVID-19 tax relief fraud case tried to date in the country — submitting over 1,900 false employment tax returns exploiting the Employee Retention Credit with fictitious employee counts and fabricated wages, fraudulently seeking more than $170 million and pocketing over $55 million before being convicted in November 2025 and sentenced in April 2026 to 12 years in prison and $55 million in restitution.

Case 2: A Florida CPA Who Should Have Known Better — $2.2 Million Evaded

In a separate case, Ronald St. Clair, a Florida-licensed CPA, pleaded guilty in April 2026 to evading more than $2.2 million in income taxes (tax years 2011–2017) by selling real property and funneling the proceeds through a third party’s account to hide them from the IRS — all while simultaneously negotiating a payment plan with the agency. Together, these cases underscore that credentials create accountability, but the absence of any oversight for uncredentialed preparers leaves taxpayers with virtually no protection at all.

Congress Is Finally Moving — The TAS Act

In March 2026, Senate Finance Committee Chair Mike Crapo (R-Idaho) and Ranking Member Ron Wyden (D-Oregon) introduced the bipartisan Taxpayer Assistance and Service Act (TAS Act). The AICPA supports the bill, which includes landmark provisions for preparer regulation:

- Requires unlicensed return preparers to undergo more rigorous training and certification

- Expands the definition of “return” for preparer penalty purposes to include documents that merely purport to be returns — closing the loophole that let bad actors alter returns after signing without penalty

- Makes ghost preparer behavior a felony: willfully failing to furnish a valid PTIN would be punishable by up to $50,000 in fines or two years in prison

- Increases existing penalties — for example, the penalty for failure to sign a return would jump from $60 to $250 per offense, with a maximum of $50,000

- Raises due-diligence penalties from $635 to $1,000 per occurrence with no maximum cap

The National Taxpayer Advocate has said the TAS Act “strikes a reasonable balance between safeguarding taxpayers and minimizing undue burdens on tax preparers.”

What This Means for You as a Taxpayer

Choosing the right tax preparer is one of the most important financial decisions you make each year. Here’s what to look for — and look out for:

Green flags — credentials that require accountability:

- CPA (Certified Public Accountant) — licensed by state boards of accountancy, subject to mandatory CPE, ethical standards, and disciplinary oversight

- EA (Enrolled Agent) — federally licensed by the IRS, must pass a comprehensive three-part exam covering all aspects of federal taxation and complete 72 hours of CPE every three years

- Attorney — licensed by state bar associations with their own ethical oversight

Red flags:

- Preparer refuses to sign the return or leaves the PTIN line blank (classic ghost preparer behavior)

- Guarantees a large refund before seeing your documents

- Charges fees based on a percentage of your refund or there are discrepancies between the refund amount and what you received in your bank account

- Pushes deductions you’ve never heard of without asking for documentation

- Doesn’t ask questions about your income, family, or business

The Bottom Line

The federal government has left a gaping hole in consumer protection by failing to mandate minimum competency standards for tax preparers. The vast majority of all registered preparers carry zero formal credentials. They are responsible for 94% of EITC dollar adjustments, 93% of all preparer penalties, and some of the most egregious fraud cases in IRS history. States like New York, California, Oregon, and Maryland are stepping into the breach — but the patchwork is no substitute for a uniform national standard.

The TAS Act, if enacted, would be a meaningful step forward. Until then, taxpayers must take personal responsibility for vetting who prepares their returns. We support the TAS Act to protect the taxpayer because your finances, your refund, and your reputation with the tax authorities are too important to leave in unqualified hands.

PS: This is not a new problem. At GG CPA Services, we have been sounding the alarm on unregulated tax preparers for years. A few examples from our prior coverage are linked below.

Most serious problems (IRS report): #5 Lack of competency of tax preparers

Tax Time IRS Guide: Select a tax return preparer with care

IRS Tips to help people choose a reputable tax preparer

Thomson Reuters article on the Mystery shopper report from Center for Taxpayer Rights – New Report Fuels Calls to Regulate Uncredentialed Tax Preparers